The Psychology of Financial Goals: Why Some People Stay Motivated, and Others Give Up

Setting financial goals is often presented as the first step towards financial success. Save for an emergency fund, pay off debt, invest for retirement, buy a home – these are all sensible objectives that appear regularly in financial education. Yet, despite having clear goals, many people struggle to stay committed over time.

This is not necessarily because the goals themselves are unrealistic. More often, it is because the way we think about goals does not always align with how human motivation actually works.

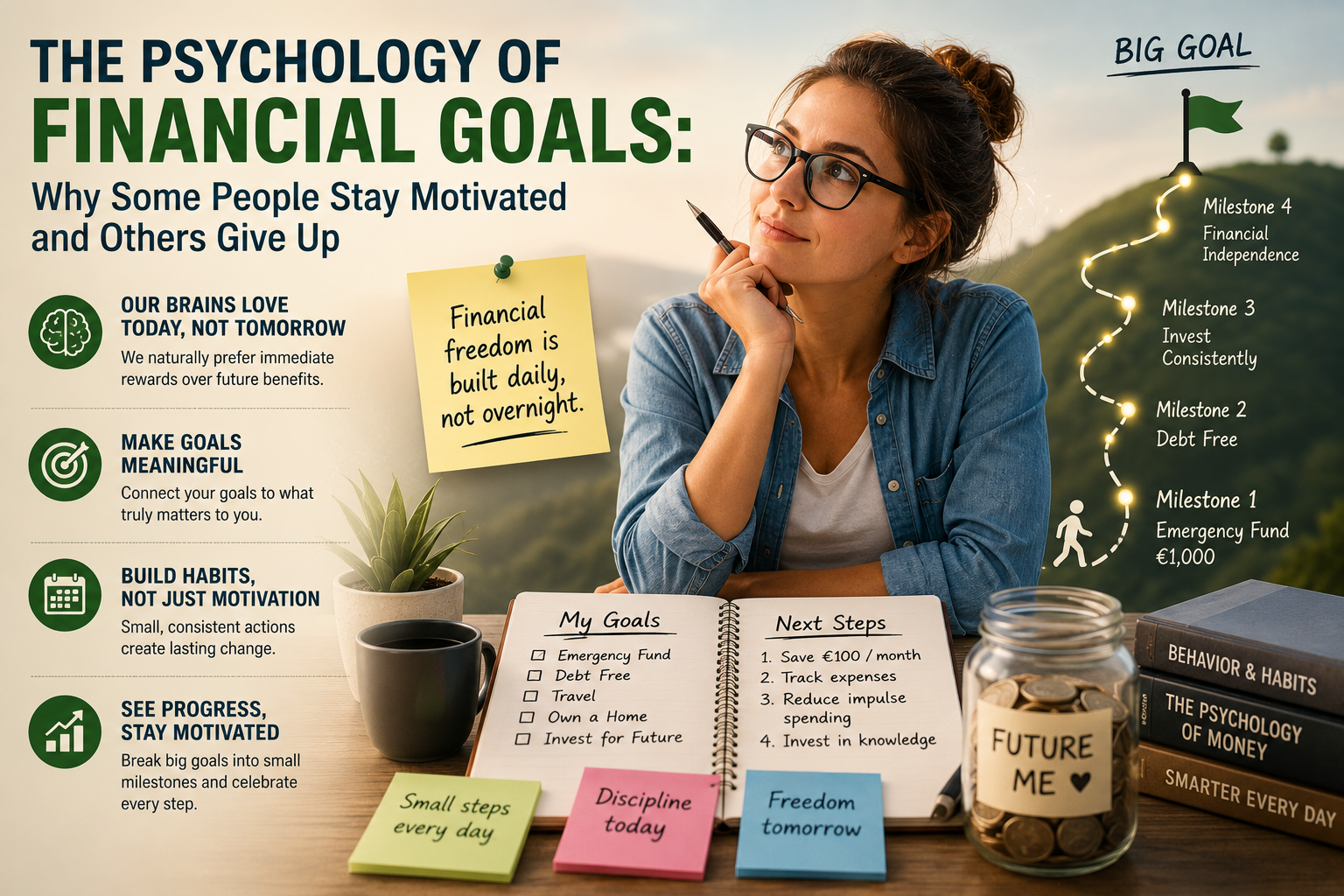

Financial goals are, by nature, future-oriented. They require people to make sacrifices today for benefits they may not experience for months or even years. While this sounds logical, our brains are wired to value immediate rewards much more highly than distant ones. Psychologists refer to this tendency as delayed gratification – the ability to resist a short-term temptation in favour of a larger future benefit.

For many people, this is where the challenge begins. The satisfaction of buying something today is immediate and tangible. The satisfaction of building an emergency fund or saving for retirement is abstract. It exists somewhere in the future, making it much harder to feel emotionally rewarding in the present.

This is why financial goals often lose momentum. At the beginning, motivation is high. People create budgets, open savings accounts, or make ambitious plans. But as weeks pass and progress seems slow, enthusiasm begins to fade. The goal remains important, yet it no longer feels urgent or exciting.

Another reason many financial goals fail is that they are often too vague. Statements such as “I want to save more money” or “I should be better with my finances” express good intentions, but they do not provide a clear sense of purpose. Without a specific reason behind them, these goals are difficult to maintain when everyday life becomes busy or unexpected expenses arise.

By contrast, goals that are emotionally meaningful tend to be much more resilient. Saving for a child’s education, achieving financial independence, starting a business, or having the security to handle unexpected emergencies all carry a personal significance that goes beyond the numbers. These goals are connected to identity, values, and aspirations, making them easier to prioritise over time.

However, even meaningful goals require more than motivation. They require habits.

Motivation is powerful, but it is also temporary. It fluctuates depending on mood, energy, and circumstances. Habits, on the other hand, operate almost automatically. Setting aside a small amount of money every month, reviewing personal finances regularly, or pausing before making an impulse purchase are examples of routines that gradually reduce the need for constant willpower.

This distinction is important because long-term financial success is rarely built on occasional moments of inspiration. Instead, it is the result of consistent behaviours repeated over months and years.

Progress also plays an important psychological role. People are more likely to stay motivated when they can see that they are moving forward. Large financial goals can sometimes feel overwhelming because the finish line appears too far away. Breaking them into smaller milestones creates regular opportunities to experience success, reinforcing positive behaviour and encouraging continued effort.

This understanding has important implications for financial education. Teaching people how to calculate interest or prepare a budget is valuable, but it addresses only part of the challenge. Equally important is helping learners understand how motivation changes over time, how habits are formed, and how emotions influence financial choices.

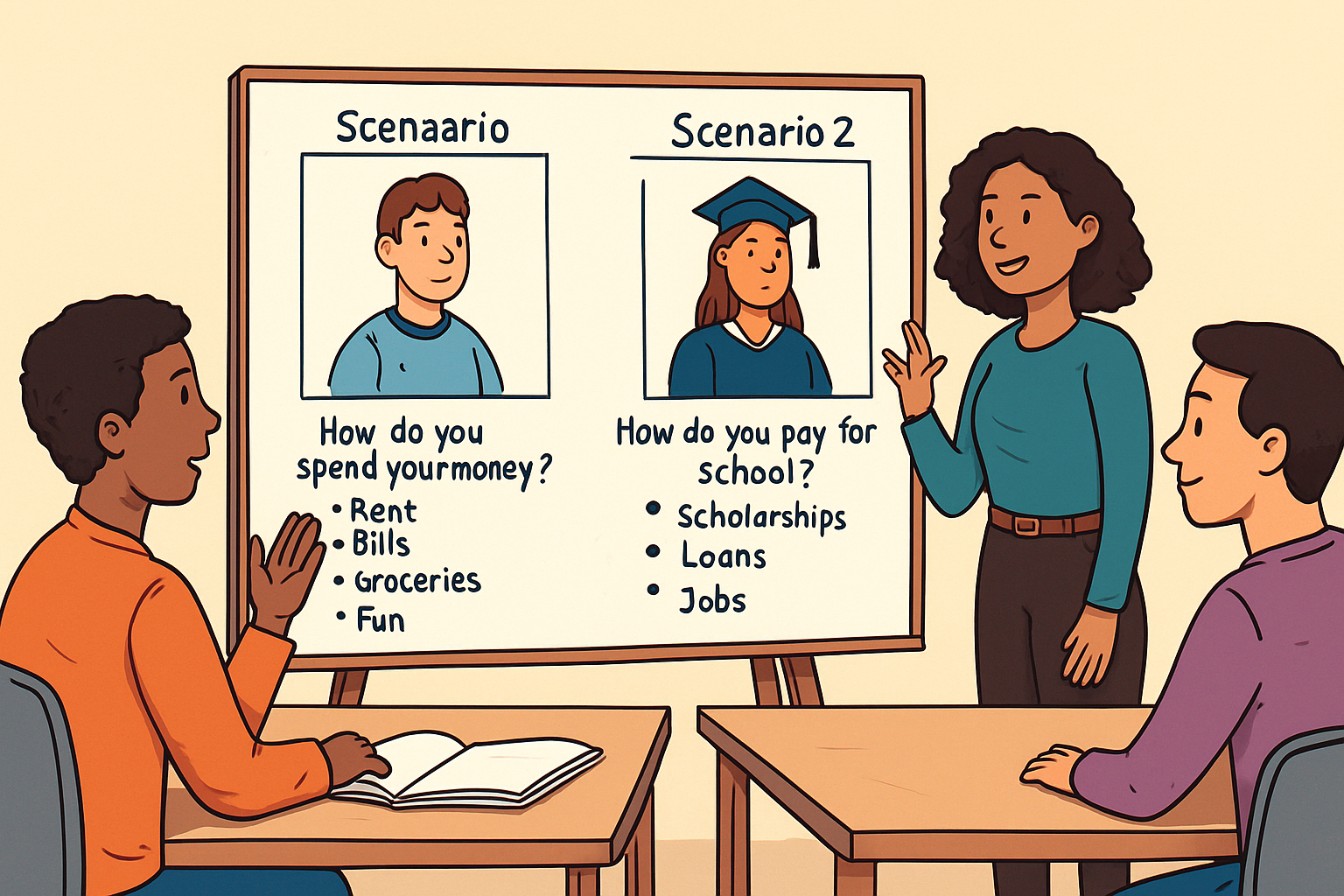

Within the FINMAN+ project, these behavioural aspects are integrated into the learning process through scenario-based education. Rather than presenting financial concepts in isolation, learners are encouraged to engage with realistic situations that reflect the decisions they face in everyday life. By exploring the consequences of different choices and reflecting on their own motivations, participants develop not only financial knowledge but also greater self-awareness and confidence.

Ultimately, achieving financial goals is not simply a matter of discipline or determination. It is about creating goals that matter personally, building habits that support them, and recognising that lasting progress comes from small, consistent actions rather than occasional bursts of motivation.

Because financial success is rarely the result of one big decision. More often, it is the product of many small decisions that continue long after the initial motivation has disappeared.